Role of Building Material Industry in Achieving Low Carbon Growth

Sakshi Nathani, March 7, 2024

With rapid urbanisation and industrialisation, the industry sector is poised for substantial growth given flagship initiatives including Make in India, AtmaNirbharBharat, Housing for All, Smart Cities, etc. that are expected to promote manufacturing in the country. Estimates suggest that about 70% of India’s infrastructure is yet to be built. In the next two decades, the total residential floor space is expected to see a massive increase from 20 billion sq. m to 50 billion sq. m.(IEA, 2021). This indicates huge opportunities to save embodied emissions from the whole life cycle of building materials or other products. The emissions from building materials and construction are irreversible once a building has been built.

Estimates suggest that 40-50% of resources extracted across the world are used for infrastructure, construction, and housing (Brown et al., 2018). About 20-25% of India’s energy demand comes from the building materials manufacturing industries (Praseeda et al., 2015). The manufacturing of building materials is both a resource and energy-intensive process. Cement and steel production are the primary sources of these emissions due to their intensive manufacturing processes and widespread usage. Subsequently, other commonly used building materials like aluminium, glass, and insulation materials also contribute towards emissions. India is the second largest producer of steel and cement in the world. The foundation of construction in India’s buildings largely relies on reinforced concrete and steel frames. Around 60 million tonnes of cement and 14 million tonnes of steel were used for urban construction in India in 2020 (PIB India, 2021). The construction sector primarily drives the demand for steel, particularly in housing and commercial spaces. In 2022, this sector accounted for 45% of the steel demand, a this is expected to increase up to 60% by 2030. Similarly, cement demand in the country is significantly influenced by the housing sector. Urban housing contributes approx 25-26%, rural housing around 28-30%, and government-led initiatives such as the low-cost housing PMAY schemes add another 11-12% (Probe42, 2020). Aluminium is widely used in building and construction due to its inherent properties like lightness and corrosion resistance. In 2022, the demand for primary and secondary aluminium stood at 15-17% and 21- 22%, respectively, within the sector (CRISIL, n.d.). Considering the current rate of urbanisation and various government initiatives such as Make in India, Housing for All, and Smart Cities, the demand for major building materials is expected to grow substantially in the coming decades.

Estimates suggest that about 70% of India’s infrastructure is yet to be built. In the next two decades, the total residential floor space is expected to see a massive increase from 20 billion sq. m to 50 billion sq. m.

With rapid urbanisation and industrialisation, the industry sector is poised for substantial growth given flagship initiatives including Make in India, AtmaNirbharBharat, Housing for All, Smart Cities etc. that are expected to promote manufacturing in the country. Estimates suggest that about 70% of India’s infrastructure is yet to be built. In the next two decades, the total residential floor space is expected to see a massive increase from 20 billion sq. m to 50 billion sq. m.(IEA, 2021). This indicates huge opportunities to save embodied emissions from the whole life cycle of building materials or other products. The emissions from building materials and construction are irreversible once a building has been built.

Estimates suggest that 40-50% of resources extracted across the world are used for infrastructure, construction, and housing (Brown et al., 2018). About 20-25% of India’s energy demand comes from the building materials manufacturing industries (Praseeda et al., 2015). The manufacturing of building materials is both a resource and energy-intensive process. Cement and steel production are the primary sources of these emissions due to their intensive manufacturing processes and widespread usage. Subsequently, other commonly used buildingmaterials like aluminium, glass, and insulation materials also contribute towards emissions. India is the second largest producer of steel and cement in the world. The foundation of construction in India’s buildings largely relies on reinforced concrete and steel frames. Around 60 million tonnes of cement and 14 million tonnes of steel were used for urban construction in India in 2020 (PIB India, 2021).

The construction sector primarily drives the demand for steel, particularly in housing and commercial spaces. In 2022, this sector accounted for 45% of the steel demand, a this is expected to increase up to 60% by 2030. Similarly, cement demand in the country is significantly influenced by the housing sector. Urban housing contributes approx 25-26%, rural housing around 28-30%, and government-led initiatives such as the low-cost housing PMAY schemes add another 11-12% (Probe42, 2020). Aluminium is widely used in building and construction due to its inherent properties like lightness and corrosion resistance. In 2022, the demand for primary and secondary aluminium stood at 15-17% and 21- 22%, respectively, within the sector (CRISIL, n.d.). Considering the current rate of urbanization and various government initiatives such as Make in India, Housing for All, and Smart Cities, the demand for major building materials is expected to grow substantially in the coming decades.

Transitioning to a future of low-carbon built environments requires the design of multi-beneficial material strategies that take a whole building life cycle and a systems-thinking approach

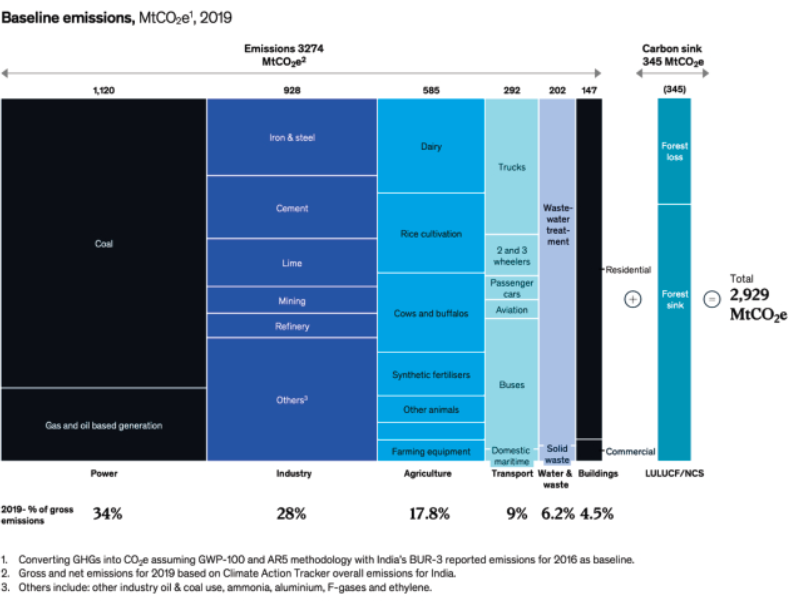

Transitioning to a future of low-carbon built environments requires the design of multi-beneficial material strategies that take a whole building life cycle and a systems-thinking approach. Embodied Carbon emissions have not been addressed at the same scale as operational emissions and energy efficiency improvements in India. Operational carbon emissions can be reduced over time by decarbonising the electricity grid and energy efficiency retrofits. India’s commitment to achieve net zero emissions by 2070 includes interim targets for the power sector as well as a separate voluntary pledge for the transport sector. However, for the industry sector consuming around 50% of total energy, essentially through fossil fuels, a clear transition path towards emissions mitigation needs further analysis. Comprehensive sector-level decarbonisation strategies and roadmaps are necessary to establish the groundwork for future scaling and to attain substantial reductions in GHG emissions. The process of reducing carbon emissions within the buildings sector’s portfolio also drives sustainability in the industries upstream and downstream in the value chain.

The government and the financial sector have a pivotal role to play in decarbonizing the industrial sector. India’s existing industrial policy frameworks currently prioritise rapid growth, energy security and enhancing competitiveness. Energy efficiency, fuel switching, process modifications, electrification by renewables, material circularity and substitution, and resource efficiency are important levers for decarbonising industrial sectors. The primary focus is on low-hanging levers such as energy efficiency and renewable energy which are insufficient to drive the transition towards low carbon growth. Energy efficiency is often referred to as the ‘first fuel’ for decarbonisation. It is the easiest and most costeffective way to address climate change, facilitate transitions to renewable energy, provide reliable and affordable energy access, support low-carbon economic growth, enhance the security of supply, and reduce dependency on imported energy sources. Although its contribution to the overall pathway to achieve Net Zero is approximately 25% (IEA, 2021).

Existing Policy Landscape for Hard-to-Abate Sectors

Industrial operations and infrastructure encompass a diverse array of processes, materials, and technologies. Achieving low-carbon industrial growth and contributing to global climate change mitigation requires crucial elements such as enhancing energy and material efficiency, substituting processes and fuels, embracing circular economy principles, adopting renewables, and integrating low-carbon fuel solutions. Energy efficiency remains a cornerstone of India’s overall strategy for lowcarbon development. Current policies and programs under these elements are outlined below:

- Enhancing Energy Efficiency

- Perform, Achieve and Trade (PAT) Scheme for

Industries

The PAT scheme is the flagship programme of the National Mission for Enhanced Energy Efficiency. It is implemented by the Bureau of Energy Efficiency (BEE) under the aegis of the Ministry of Power. The PAT Scheme is a regulatory instrument for reducing the specific energy consumption (SEC) of energy-intensive industries by allocating SEC targets and allowing the trading of certificates (called Energy Savings Certificates, or ESCert). It is a completely market-based mechanism, focused primarily on enhancing the energy efficiency of large energy-intensive sectors by adopting low carbon efficient technologies. A total of six cycles of the PAT scheme have been launched till April 2020, covering 1073 industries from 13 industrial and service sectors, which represents about 50% of the primary energy consumption of India. The seventh cycle had been notified in October 2021 for the next three years.

This scheme identifies designated consumers (DCs) across select energy-intensive industries who must meet mandated energy efficiency targets in each period and failing to achieve the targets leads to a penalty. The cement industry has been part of PAT cycles since its inception in 2012, and in every cycle, the industry has been able to overachieve its reduction targets. In PAT cycle I, it was able to overachieve the target by 82% and in PAT cycles II and III, it was able to overachieve by 49% and 75% respectively. In the iron and steel sector, a total of 5.013 Mtoe of energy savings were achieved between 2012 and 2020 under the PAT scheme, amounting to total GHG emission reductions of 18.64 million tonne CO2eq. Similarly, 12 designated consumers from the aluminium industry successfully achieved an emissions reduction of 5.24 MtCO2 between 2016 and 2019 (BEE, n.d.). PAT scheme has kicked off an energy efficiency drive in India. India plans to build upon the PAT scheme with a focus on energy-efficient technologies, and the needs of MSMEs in the subsequent phases.

Energy Conservation & Building Code

To improve the energy efficiency of new commercial buildings, the Energy Conservation Building Code (ECBC) was launched in 2007 by the Ministry of Power. ECBC establishes the minimum energy standards for commercial buildings with a connected load of 100 kW or a contract demand of 120 kVA and higher. While the Central Government has authority under the EC Act of 2001, state governments have the flexibility to adapt and notify the code according to their specific local or regional requirements. Currently, the code is in a voluntary phase of implementation, and approximately 22 states are in different stages of making ECBC mandatory. The code underwent a significant update in 2017, with an increased focus on promoting occupant comfort through passive design strategies and daylight integration. It remains technologically neutral while encouraging renewable energy adoption and with emphasising a building’s life cycle cost. It is observed that with the voluntary energy performance levels as specified in the code, the resulting energy savings are 25-50% over the conventional structures.

Enhancing Material Efficiency & Recycling

In the steel sector, the utilisation of scrap is an important strategy to reduce emissions. The Steel Scrap Policy introduced in 2019 aims to promote a circular economy; minimize dependency on imports; and ensure proper and scientific handling, processing, and disposal of all types of recyclable scraps. Indian steel industry aims to create 300 MT of demand by 2030, with a contribution of 35-40% from the EAF/IF route, with scrap as an input.

Renewable Energy Integration

Electrification through renewables can have a significant impact on overall emissions. The Renewable Purchase Obligation mechanism was introduced as part of the Electricity Act 2003 to create demand for renewable power. The targets are set by the regulated entities – electricity distribution companies for large power consumers- like steel and cement industries that are expected to procure a minimum percentage of the total consumption of electricity from RE sources. Renewable Energy Certificate (REC) is the tradable instrument used under the scheme.

Planned Initiatives

With the recent amendment of the Energy Conservation Act in 2022, major programs under the Ministry of Power’s Bureau of Energy Efficiency (BEE) have undergone significant enhancements. This amendment mandates the use of renewable energy and carbon-neutral technologies, as well as the inclusion of sustainability aspects across sectors. Specifically, it has integrated renewable energy and green building requirements into the Energy Conservation Building Code (ECBC), transforming it into the Energy Conservation & Sustainable Building Code (ECSBC). This updated code is expected to encompass various sustainability aspects, including material and resource efficiency, clean energy deployment, and circularity. Additionally, the amendment now applies ECSBC norms to all residential buildings with a minimum connected load of 100 kW or contract demand of 120 kVA.

Energy Conservation Act of 2022 aims to establish a domestic carbon market and implement a carbon trading mechanism to fulfil India’s climate mitigation commitments.

Furthermore, the Energy Conservation Act of 2022 aims to establish a domestic carbon market and implement a carbon trading mechanism to fulfil India’s climate mitigation commitments. To address barriers in the issuance and trading of Energy Savings Certificates (ESCerts), there’s a proposed framework transition from tonnes of oil equivalent (ESCerts) to carbon credits expressed in tonnes of carbon dioxide (CO2) equivalent. The plan involves phased implementation, starting with a voluntary market to stimulate demand for existing instruments (ESCerts and RECs, which will be converted to carbon credits). Subsequently, credits will be supplied through project-based registration and issuance, culminating in the establishment of a compliance cap-and-trade market. Timely integration of energy efficiency, renewable energy, and sustainability aspects into all new construction will help in achieving 2070 NZ targets.

Mandating consumption of non-fossil sources will potentially reduce India’s fossil fuel imports and enhance energy security. Major sectors like mobility and industrial production are significantly dependent on imported fossil fuels. The National Green Hydrogen Mission, approved in January 2023, aims at making India the Global Hub for production, usage and export of Green Hydrogen and its derivatives. Green hydrogen, produced using renewable energy, has the potential to play a key role in achieving lowcarbon and self-reliant economic pathways. Green hydrogen has the potential to harness locally abundant renewable energy resources throughout different regions and seasons. It can serve various purposes, functioning as a fuel or industrial feedstock, and can directly substitute fossil fuel-derived feedstocks, such as in steel manufacturing thereby reducing emissions.

Way Forward:

Existing policy levers aimed at increasing energy efficiency, such as the Perform Achieve and Trade (PAT) Scheme, or for promoting greater resource efficiency and material circularity, such as the Steel Scrap Recycling Policy. They will play an important role in halting the growth of emissions in the shortterm – till 2030. However, they will be inadequate for achieving the deep decarbonization required in the medium to long term. As per the sectoral roadmaps of most countries, low-carbon technologies like hydrogen and Carbon capture, utilisation and storage (CCUS) will play a crucial role in decarbonising the manufacturing process of emission-intensive building materials in the long term. While these technologies exist, most are currently under development, commercially unviable and have a significant cost of abatement. Given the projected 3-4X rise in demand for these materials by 2050, it is imperative for all stakeholders to take early actions to ensure lowcarbon capacity addition and avoid carbon lock-in. There has been growing ambition from businesses across the built environment value chain, with leading companies announcing net-zero commitments. Manufacturers are introducing building materials with reduced carbon content, aiming to both mitigate climate change risks and capitalize on the significant opportunities that emerge as the global economy transitions towards net-zero emissions. Dalmia Bharat Cement, Ultra Tech Cement, ACC Cement, Ambuja Cement, Steel, Saint-Gobain, and Berger Paints are a few of the Indian companies with net-zero carbon roadmaps and environmental product declarations for their products. Effective policy frameworks that include a mix of fiscal, financial, market-based, and regulatory interventions that target both the supply side and demand side are needed to promote low carbon growth of steel & cement sectors, also regarded as ‘hard to abate’ sectors.